Abstract

The past years bankruptcy filings are higher than ever. According to Knegt, Beukelman, Popma, van Willigenburg and Zaal (2005) bankruptcy fraud is present in 25% of all bankruptcy cases in the Netherlands. Damages are estimated as high as €1.500.000 per year (Veldkamp & de Vries, 2008). This paper attempts to find variables that correlate with bankruptcy fraud. Data was collected in collaboration with the Public Prosecution Office. Eleven datasets are used. The largest of these consists out of 1121 companies and the smallest one out of 194 companies. A correlation with bankruptcy fraud is found with the number of changes in management the six months prior to bankruptcy and with the number of financial antecedents that have been committed by the owner(s). There is also a strong correlation between registration in internal registers and the suspicion of fraud. There was no significant correlation between personality traits and bankruptcy fraud. An interesting topic for further research is the difference between the offender that commits fraud within the bankruptcy and the offender that purposefully commits bankruptcy fraud.

Samenvatting

Het aantal faillissementenaanvragen is de laatste jaren hoger dan ooit1. Volgens Knegt, Beukelman, Popma, van Willigenburg and Zaal (2005) komt faillissementsfraude voor in 25% van alle faillissementen in Nederland. De schade wordt geschat op €1.500.000 per jaar (Veldkamp & de Vries, 2008). Dit onderzoek poogt indicatoren van faillissementsfraude te vinden. De data is verkregen in samenwerking met het Openbaar Ministerie. Er zijn elf datasets gebruikt. De grootste van deze bestaat uit 1121 bedrijven en de kleinste uit 194 bedrijven. Er correleren twee variabelen met faillissementsfraude. Het aantal wijzigingen in management de zes maanden voor het faillissement en het aantal financiële antecedenten van de bestuurders. Er is ook een relatie gevonden tussen registratie in interne systemen en de verdenking van fraude. Er is geen correlatie gevonden tussen persoonlijkheidskenmerken en faillissementsfraude. Interessant voor toekomstig onderzoek is het verschil tussen de mensen die binnenin een faillissement fraude plegen en tussen diegenen die bewust en met voorbedachte rade een bedrijf opzetten of overnemen om faillissementsfraude plegen.

Table of Contents.

Abstract ii

Samenvatting ii

Introduction 4

Review of the Literature 5

White Collar Crime 6

Bankruptcy Fraud 10

Method 14

Data 14

Using Data for Hypotheses 16

Analysis 17

Results 17

Discussion 24

Limitations and Future Research 26

Conclusions 28

References 29

Introduction

Bankruptcy fraud can be defined as “purposefully and illegally acting in a way that leaves bankruptcy creditors of the bankrupt corporation financially disadvantaged” (Knegt, Beukelman, Popma, van Willigenburg & Zaal, 2005). It is a crime that often has serious financial consequences for the people involved with the bankrupted company. Former employees can be owed several months of salary arrears . Creditors do not see payment for goods or services. Taxes are no longer paid.

Bankruptcy fraud can come in different forms but there is one important distinction to make. On the one hand there are bankruptcy cases where there is the preconceived intention to start or use the company for bankruptcy and profit from it. This is the most severe form of bankruptcy fraud. On the other hand are the cases where bankruptcy is unavoidable but where it is being misused to the owners own benefit. For example, an owner who knows he is going bankrupt can sell his inventory at a price that is far lower than the market price to a friend instead of letting it be seized in bankruptcy to pay off debts. These two forms of fraud are ends at a scale. In the middle of these two is a large gray area where there is a mixture of both.

If we take into account all forms of bankruptcy fraud, it is estimated that the occurrence rate is 25% in all bankruptcies in the Netherlands (Knegt et al. 2005 p.12). It is difficult to accurately indicate the damage that this type of fraud causes, but estimates are up to €1.500.000.000 per year (Veldkamp & de Vries, 2008) or even higher. The people that commit these crimes are hard to prosecute because they often use straw men or dummy corporations to take the fall for them. The probability of detection and prosecution is only 2,5%. This low rate is partly because the police department does not have enough staff to examine every single bankruptcy case for signs of fraud. Therefore, the cases where the probability of bankruptcy fraud is highest are selected for further investigation.

In order to select the cases with the highest risk of bankruptcy fraud there is a need for factors that are indicators of it. There are two studies that give specific handles for indicators of bankruptcy fraud. Knegt et al. (2005) give an extensive overview on the problem of bankruptcy fraud in general. They point out a number of organizational variables that are indicators of fraudulent activities. Veldkamp and de Vries (2008) use a mathematical approach to find correlations between personal characteristics (such as owners crime record) and bankruptcy fraud. These findings can be used to raise the detection rate (although they have yet to be implemented) and to arrive at a more effective way of battling the bankruptcy fraud problem.

Another trend that has been developing the past decade is to look for differences in the personality of managers of CEO’s that do and do not commit fraud. It has been shown that in general people with certain personality traits are more likely to commit fraud than others (Alalehto, 2003. Smith, 2004. Blickle, Schlegel, Fassbender & Klein, 2006. Pogrebin, Poole, & Regoli, 1986). If it is known which personality traits cause a person to be at high risk for committing bankruptcy fraud, those traits can be used as another indicator.

As of yet there is no research that gives a clear personality profile specifically for bankruptcy fraud offenders. That means that the question which people –when all other circumstances are equal– commit bankruptcy fraud and which do not is unanswered. An answer to this question could help the police department be even more successful in predicting the cases where bankruptcy fraud takes place.

The research question of this paper focuses on finding the indicators that hint at the presence of bankruptcy fraud. The focus lies both on organizational variables and on personal variables such as personality determinants and bio data. This knowledge combined with the indicators from previous studies may improve our effectiveness in identifying bankruptcy fraud.

Review of the literature

The amount of research that focuses on bankruptcy fraud is very limited and there is no research that specifically looks at its relationship with personality traits. However there are some studies that direct their attention to the relationship between personality traits and the more general ‘white collar crime’ topic. Because bankruptcy fraud falls within the scope of white collar crime we use the working hypothesis that findings on white collar crime can be extrapolated towards bankruptcy fraud. We begin by reviewing the literature on the wider subject of white collar crime and its correlation with personality and bio data and work towards the literature that is directed specifically on bankruptcy fraud.

White collar crime.

There is no universally accepted definition of white collar crime. The first attempt to define it comes from Sunderland (1940). He defines it as a crime “committed by a person of respectability and high social status in the course of his occupation”. There has been much debate over this definition. Benson & Simpson (2009) make a good point when they say that the emphasis should simply be put on the fact that white collar crimes are often committed by persons with a high social status and that the offence is usually occupationally related but a clear definition helps us to delineate the subject. Edelhertz (1970) defines white collar crime as: “an illegal act or series of illegal acts committed by non-physical means and by concealment or guile, to obtain money or property, to avoid the payment or loss of money or property, or to obtain business or personal advantage”. This definition is preferred because it is less strict and allows for a wider range of crimes including bankruptcy fraud to fall within the scope of white collar crime.

White collar crime can be subdivided into multiple categories. Coleman (2002) describes six. One of them is ‘fraud’ and bankruptcy fraud can be placed within this category. The other five are employee theft, embezzlement, ‘computer crime and deception’, ‘bribery and corruption’ and ‘conflict of interest’.

In the first studies on white collar crime the general assumption was that the factors correlating with fraud are found in organizational factors (such as company size, branch etc. See for instance Zahra and Pearce (1989)) and in the available fraud opportunities that managers have. There was little attention to personal differences between managers (Elliot, 2010). This leaves the question open why some employees do commit fraud and others do not when all other circumstances are equal. This question has become the focus of research more often in the past decade. Researchers started to shift their focus from the organizational factors towards the personality traits of white collar offenders. (Alalehto, 2003. Smith, 2004. Blickle et al., 2006. Pogrebin et al. 1986).

The personality of offenders has been measured with several models. Two of these studies use (parts of) the ‘Big Five’ model which distinguishes between extraversion, neuroticism, agreeableness, conscientiousness and openness to experiences(Alalehto, 2003. Blickle et al. 2006).

In his study Alalehto (2003) compares tax-evasion offenders with non-offenders using a modified version of the big five personality scale. In addition to the regular five personality traits, he adds ‘negative valence’ (evil vs. decent) (Almagor, Tellegen, & Waller, 1995). He finds a tendency that persons who have a dominating personality trait that is either extravert, neurotic or disagreeable are more likely to commit an economic crime. In other words people who score high on one of these three traits have a higher risk of committing fraud. The extraverts are the most sympathetic persons in his offenders-list. With their outgoing character and social competency they have the possibility to use their extrovert energy to manipulate others. People who score high on ‘disagreeable’ as their dominant personality trait are also at risk. Their actions are often more straightforward because they are not able to manipulate in the same way the positive extrovert does. The last risk factor Alalehto finds is a high score on ‘neuroticism’. He calls these ‘the neurotic’. The neurotic turns his anger and disappointment inwards, causing unbalanced behavior and mood-swings. This in turn sets him at risk for fraudulent behavior. Alalehto does not give an explanation why people who fall in one of these categories have a higher risk to commit fraud than those that fall in multiple categories but because of his small number of test subjects (N=128) it is likely that there are simply too few people that fall into multiple categories to make reliable statements on.

The other study that takes into account a factor of the ‘Big Five’ is done by Blickle et al. (2006). High-ranking managers that have been convicted of white collar crime are compared with their non-convicted peers. Several different scales are used for measurement of personality. One of the traits measured is conscientiousness. The other scales measure hedonism, narcissism, social desirability and self control. Their findings indicate that convicted managers score higher on conscientiousness, hedonism and narcissism and lower on behavioral self-control than their non-convicted colleagues. The finding that offenders score higher on conscientiousness is surprising and contradicts earlier research (Kolz, 1999). An explanation is that managers need a high technical proficiency to attain their job. A trait that can be expected more often in those with high conscientiousness. The higher their technical proficiency, the lower the perceived risk of getting caught, making the crime more attractive. Low scores on integrity or low self-control add further to the probability of committing fraud. Therefore scores on a personality-based integrity test (better known as honesty scales) are negatively correlated with anti-productive behaviors such as stealing (Ones & Viswesvaran, 2001).

Recently a review has been released by Ragatz & Fremouw (2010) in which they critically examine sixteen papers concerning several forms of white collar crime. They focus solely on studies that examine the individual variables. Six of the sixteen studies deal with psychological variables. Their conclusions are that in general “white-collar offenders are older, Caucasian, employed, and have a high school diploma or higher education. They also tended to be low in conscientiousness, agreeableness, and self-control“. They also note that a drawback in the current literature is the fact that there is no research that focuses on differences between men and woman. Based on earlier studies it is likely that there will be some differences between the two groups. Ragatz and Fremouw (2010) come to their conclusions by reviewing all studies on white collar criminals they could find and by analyzing all of the conclusions in these publications. They assume that the population of white collar criminals is homogeneous. This is an assumption that should not be made too easily. Because of some of the conflicting data in different research it is likely that not all white collar criminals are the same. It might be more valid to look at groups that commit similar kind of white collar crimes.

Hypothesis 1

“Offenders guilty of bankruptcy fraud score lower on self control than non offenders.”

Hypothesis 2

“Offenders guilty of bankruptcy fraud score lower on conscientiousness than non offenders.”

Blickle et al. (2006) also compare the bio data from convicted white collar criminals with regular non-convicted white collar professionals. They found that the offenders were on average 46.8 years and had a mean income of €66.169 the year before they got imprisoned. Managers who were not convicted on the other hand were on average 44.1 years old and had a mean income of €105.000. The difference in income is most likely caused by ongoing investigations that can take several years prior to the actual imprisonment and that can hinder in the work hemisphere. Because of this they do not draw any conclusions regarding income differences between white collar criminals and non-criminals.

Hypothesis 3

“Offenders guilty of bankruptcy fraud are older than non-offenders.”

There is another study (Pogrebin et al. 1986) that takes bio-data into account. They arrive at different conclusions. Pogrebin et al. (1986) find a mean income of $10,000. Unfortunately they used no control group, making it impossible to compare this data to similar employees who did not embezzle. However, the difference in income when compared to the study by Blickle et al. (2006) is striking. There may be several reasons for this difference. First there is the time and place of the study. The study by Pogrebin et al. was conducted in 1986 in the United States, Colorado. The mean income at that time and place was $30.256. In Germany the average gross income in 2006 was €42.382 (when transformed at the dollar vs. euro rates at that time: $53.743) Secondly, a large portion (79%) of the respondents were female (vs. 7,9% at Blickle et al. 2006) who had a lower income. The biggest difference however lies in the type of white collar crimes the subjects committed. In the study conducted by Blickle et al. (2006) they interviewed top-managers who were at the peak of their careers (average age of 46,9 years) and who committed “high-level white collar crimes”. Their definition of “high level white collar crimes” consists out of those crimes that are committed by a corporate manager, a high ranking technical specialist, an official representative of a corporation or the owner of a corporation. Included with these crimes is fraudulent bankruptcy. In contrast, Pogrebin et al. (1986) studied employees who for the most part worked at low entry levels and over half of them were in their first year of employment. The average age was 26 years. These findings imply that Blickle et al. (2006) and Pogrebin et al. (1986) are conducting research on different white collar crimes. The first looks at convicted offenders of various crimes including fraudulent bankruptcy (others are: bribery, counterfeiting, embezzlement, forgery, fraud, smuggling, and tax evasion), while the latter puts the focus on people convicted of embezzlement. This is an example of the point mentioned earlier. Not all groups of white collar criminals should be seen as homogenous.

Finally, there is a recently released paper by Elliot (2010) where she advocates a different direction. She believes that making use of the ´Big Five Model´ an approach that is too theoretical. She advocates the use of the Type A/B model (Friedman & Rosenman, 1994). Her main argument is that the ‘Big Five’ test is too abstract. It does not give concrete indicators. The Type A/B approach is aimed more at behavior and should therefore be better measurable. The Big Five model is backed up by research that supports its validity but it only gives scores on theoretical constructs. These scores are not directly observable and will be unknown in most cases. Because of this, we have to derive the scores from behavior or other observable variables which can be difficult, inaccurate or impossible. The type A/B model on the other hand already describes the different behaviors that both types would exhibit. Because the knowledge we have of the people under investigation is often limited it might be more constructive to search for behavior that indicates Type A or B persons than using known data to search for personality determinants which are often very abstract. Two professions already use this approach, namely medicine and the military. However as of yet there is are no studies on white collar crime in relation to the Type A/B model.

Taking everything into account, there is some research available on the subject of white collar crime and its relationship with personality determinants. The fact that white collar crime is often studied as one particular type of crime with one particular type of offender causes large differences between the studies and makes it difficult to interpret and generalize the results. White collar crime is a complex construct which exists of a multitude of different crimes where each crime is executed by particular groups of offenders. A group that is likely to commit employee theft for instance is likely to possess a different set of personality determinants than offenders of fraud and deception.

Bankruptcy Fraud.

Bankruptcy fraud can be considered a form of white collar crime when using the afore mentioned definition by Edelhertz (1970) and stressing that this particular type of fraud is by definition occupationally related and often committed by persons of a relatively high social status. As mentioned before, bankruptcy fraud can –much like white collar crime– take several different forms and we make the distinction between lower level bankruptcy fraud and the premeditated higher level bankruptcy fraud.

The literature on white collar crime is focused on white collar crime in general. We have to decide which data can be extrapolated towards the topic and at which level it can be placed. Our ‘low level’ offender is the entrepreneur who abuses the situation and takes advantage of the inevitable bankruptcy. The research by Alalehto (2003), Benson & Simpson (2009) and Ragatz & Fremouw (2004) can be considered to fall in this category. Their test populations are involved with white collar crimes such as tax evasion. Conclusions can be drawn that these offenders are generally older, score low on conscientiousness and self control and have either a dominating extrovert, disagreeable or neurotic personality determinant.

This ‘lower level’ type of bankruptcy fraud can be done in three ways.

•Assets can be withdrawn from the company or can be kept from the creditors.

•Assets can be retransferred under the appearance of obligations or can be sold at a price under market value.

•Fulfilling expenditure commitments towards friendly third parties or other managers while there are other privileged creditors.

Based on these actions Knegt et al. (2005) describe behaviors that are typical for these actions that are performed within the bankruptcy (the ‘lower level criminals’). These indicators are listed in Box 1.

The group that starts or buys a company with the premeditated intention of letting it go bankrupt can be seen as a different kind of offender. This group uses a premeditated strategy to escape criminal persecution.

The study by Blickle et al. (2006) can be placed at these ‘higher level’ offenders because of its test group which consists out of high ranking managers. They also include bankruptcy fraud. Although Blickle et al. (2006) make no distinction between different kind of bankruptcy fraud offenders, we can assume that these are mostly the ‘higher level’ offenders. All of the respondents in this study are incarcerated and because punishment for the group of ‘higher level’ criminals is often more severe and leads to imprisonment more often it is likely that the offenders belong to this group. As is mentioned before, their findings are that conscientiousness is positively correlated with white collar crime. This is in contrast to other research. We suspect that this is because Blickle et al. (2006) are studying a different group, namely the ‘high level’ offender instead of the ‘low level’ offender. Other indicators that Knegt et al. (2005) find for companies that are started or bought with the premeditated intention to let them go bankrupt (the ‘higher level criminals’) are shown in Box 2.

Box 1.

Indicators of bankruptcy fraud within the bankruptcy by Knegt et al.

Box 2.

Indicators of premeditated bankruptcy fraud by Knegt et al.

Besides these organizational indicators Veldkamp and de Vries (2008) are capable of further refining their results by use of a mathematical approach and neural networks. Their biggest predictor is the criminal record of directors. Using this they predict around 30% of the fraud cases with only 3% false positives. Their analysis is done without the use the indicators mentioned by Knecht et al. (2005). Unfortunately their data does not allow them to make a distinction between the kind of fraud that is committed.

Both Knegt et al. (2005) and Veldkamp and de Vries (2008) name the involvement with previous illegal acts or bankruptcies as an indicator.

Hypothesis 4

“The bigger the owners or managers criminal records, the higher the probability for bankruptcy fraud.”

Veldkamp and de Vries also call attention to the fact that the number of changes in management in the six months prior to the bankruptcy is an indication of fraud. A lot of changes in management in the months prior to the bankruptcy can be seen as a sign that the company has been preparing itself for bankruptcy. This is an indicator that Knegt et al. mention for bankruptcy fraud as shown in Box 2.

Hypothesis 5

“The more changes in management the six months before bankruptcy, the higher the probability of bankruptcy fraud.”

Method

Data

The data is the same that Veldkamp and de Vries (2008) use in their research. At that time the Public Prosecution Service requested a statistical analysis in order to improve their approach against bankruptcy fraud. They provided eleven confidential datasets. Even though the dataset itself is confidential most of it is publically accessible through the Chamber of Commerce. Some variables however were specifically constructed for analysis and are not public data. An example of this is the amount of economic crimes an owner/manager has been convicted of.

From the eleven datasets some were related with each other. In total four groups can be formed out of the different sets. The main group consist out of five datasets. It has data on investigated bankruptcies and which companies have committed bankruptcy fraud. The second group is a single dataset. It has information on suspected bankruptcy fraud and the registration in internal systems. The third group was formed out of three datasets. It contains records on criminal offences that individuals have committed. There is some overlap with the first group of datasets. By comparing names and birth dates it is possible to merge this group with the first group of data. The fourth and last group consisted out of a sample of companies that could be used in a control group. In the study of Veldkamp and de Vries (2008) this group was used to measure the predictive powers of their model. In this research this group has no added value and is ignored.

The five datasets in the main group are on cases in the same district. The data in these sets is merged through their “Dossier Numbers”. This results in a dataset of N=1479. The dependent variable is “Bankruptcy Fraud (0/1)” with ‘0’ meaning that there is no bankruptcy fraud and ‘1’ meaning that bankruptcy fraud has been detected. There are fourteen independent variables. The variable ‘Financial Antecedents’ is categorical (‘0’=no, ‘1’=yes), The other fifteen are ratio variables. These variables are: ‘Cases Involved’, ‘Cases Convicted’, ‘Facts Involved’, ‘Facts Convicted’, ‘Economic Cases Involved’, ‘Economic Cases Convicted’, ‘Economic Facts Involved’, ‘Economic Facts Convicted’, ‘Cases Pending’, ‘Economic cases Pending’, ‘Facts Pending’, ‘Economic Facts Pending’ and ‘Changes in Management’. One case can consist out of multiple facts.

Besides the given independent variables several others were constructed. These included ‘Total Facts’, ‘Total Cases’, ‘Total Convicted Cases and Facts’, ‘Total Offences Pending’ and ‘Total’. Each variable added up two or more of the given variables to create a new variable. These were the sum scores of offences that were related to each other.

The second group consists out of a smaller number of cases (N=194). This dataset was not connected to the others. The 194 companies that filed for bankruptcy had been examined by the fraud disclosure office. The dependent variable here is not “Bankruptcy Fraud (0/1)” but “Suspected Bankruptcy Fraud (0/1)”. The value ‘0’ means that there is no suspected fraud and ‘1’ means that bankruptcy fraud is suspected by the fraud disclosure office. Independent variables are ‘Registration in BPS’, ‘Registration in HKS’ and ‘Registration in MOT’. These three systems are internal police systems. The first of these is the B.P.S. which stands for ‘Business Processes System’. All activities performed by the police are logged in this system. Neighborhood disturbance is an example of an activity that can be found in the B.P.S. The H.K.S. stands for ‘Recognition Service System’. This system only registers offences of certain categories. These consist mainly out of administrative or economic offences. The third system is named M.O.T. and is a disclosure office for unusual transactions. Financial irregularities are registered here. All three variables are categorical where ‘0’=no and ‘1’=yes.

Lastly three datasets were combined. These three held records of any offences individuals committed. These datasets were not connected to companies or dossier numbers.

The remaining two sets of data are irrelevant for this study and are ignored. The data was collected by a regional department. Cases in other parts of the country were not included. Due to its confidential nature the region cannot be disclosed.

Using Data for Hypotheses

The data was only given after the literature study was completed. For this reason the data does not connect directly to the hypotheses and not every hypothesis that we want to test is actually testable. Specifically, there are no direct variables that give scores on personality traits. It is not possible to let the subject fill out questionnaires so in order to test some of our hypotheses we have to use implicit measurements from observable data that is an indication of personality traits. As Rijsenbilt (2011) shows in her thesis on measuring a CEO’s narcissism level on basis of a company’s annual report, this is not impossible.

The first hypothesis is about the relationship between low self control and bankruptcy fraud. Because we have no direct score on self control, there is the need for an implicit measure. Kean, Maxim and Teevan (1993) find a relation between low self control and drinking and driving. Drinking and driving is one of the offences that is present in the third dataset. For each person we can generate two variables. One categorical variable where data is stored whether a person has been convicted of drinking and driving (‘0’=no, ‘1’=yes) and another ratio variable in which the total number of convictions of drinking and driving is stored. These new variables are then merged with the first dataset through names and birthdates. They are then used to test the hypothesis regarding self control.

There is also a hypothesis concerning the score on conscientiousness. To measure this we look at the number of traffic offences a person has. Conscientiousness is negatively correlated with the amount of traffic accidents (Skaar & Williams, 2005). In the same manner as is done with self control, two variables are created. One is categorical (‘0’=no traffic offences, ‘1’=traffic offences) and one ratio variable in which the total number of traffic offences is scored. These variables are merged with the larger dataset in the same way as the variables on drinking and driving.

The birth date for the managers and owners is known. The hypothesis that offenders are older than non-offenders is therefore testable. The only adjustment is that the months and days are left out of the equation because SPSS does not handle these well. Only the years are included.

Criminal records and the number of changes in a company are given and can be used directly.

Analysis

The analysis was conducted using SPSS 18. With the dependent variable being categorical (the only possible values being ‘yes’ or ‘no’) the use of the ‘Chi Square Test’ and ‘Logistic Regression’ were applicable. The ‘Chi Square Test’ is used to determine whether or not an effect exists. Logistic regression is used to determine the strength and direction of an effect.

Results

The main group is analyzed first. A ‘Chi square test’ is used to find significant effects. Significant results were found in the variables ‘Financial Antecedents’, ‘Management Changes’ and ‘Total All’. Secondly, a ‘simple logistic regression’ is applied on each independent variable separately to identify its direction and the strength on the probability of bankruptcy fraud. There are four significant effects here. These are ‘Financial Antecedents’, ‘Convicted Cases’, ‘Convicted Facts’ and ‘Management Changes’. Both results from the Chi Square Test and the ‘simple logistic regression’ are shown in Table 1.

In total the two tests found five variables that had a significant effect.

All variables of the main dataset have been analyzed, including those that were related to criminal records. The hypothesis that the probability of bankruptcy fraud is higher as the criminal record is higher is further analyzed. Four variables that had to do with offences were significant. These are ‘Financial Antecedents’, ‘Convicted Cases’, ‘Convicted Facts’ and ‘Total All’. By using the ‘multiple logistic regression’ we can examine which of these values have an added effect on the model. We start the test with the variable with the strongest effect (‘Financial Antecedents’) and work our way down to the one with the smallest effect (‘Total All’). A significant score on the ‘Omnibus Test of Model Coefficients’ is an indicator that the variable has added value to the model. The results are shown in Table 2.

Table 1. Summary on the effects of independent variables on bankruptcy fraud. | ||||||

X2 | df | B | S.D. | Wald | Exp(B) | |

Financial Ant. | 9.689** | 1 | .600 | .195 | 9.465* | 1.822* |

Cases | 30.032 | 27 | .022 | .015 | 2.106 | 1.022 |

Facts | 39.982 | 37 | .009 | .009 | 1.030 | 1.009 |

Econ. Cases | 13.104 | 13 | .016 | .047 | .111 | 1.016 |

Econ. Facts | 22.432 | 17 | .006 | .026 | .050 | 1.006 |

Convicted Cases | 27.656 | 18 | .059 | .027 | 4.877 | 1.061* |

Convicted Facts | 37.167 | 25 | .039 | .019 | 3.989 | 1.039* |

Conv. Econ. Cases | 8.749 | 10 | .059 | .062 | .931 | 1.061 |

Conv. Econ. Facts | 17.454 | 14 | .046 | .043 | 1.187 | 1.047 |

Cases Pending | 16.791 | 12 | .042 | .051 | .673 | 1.043 |

Facts Pending | 15.007 | 17 | .007 | .034 | .047 | 1.007 |

Econ. Cases Pending | 2.254 | 6 | -.167 | .201 | .690 | .846 |

Econ. Facts Pending | 4.665 | 9 | -.029 | .060 | .233 | .971 |

Management Changes | 39.595*** | 6 | .387 | .076 | 25.809 | 1.473*** |

Conv. Cases and Facts | 19.483 | 17 | .028 | .026 | 1.148 | 1.028 |

Total Facts | 94.289 | 74 | .003 | .003 | 1.391 | 1.003 |

Total Pending | 17.874 | 22 | .001 | .015 | .009 | 1.001 |

Total Cases | 57.503 | 45 | .009 | .007 | 2.000 | 1.009 |

Total All | 110.695* | 82 | .003 | .003 | 1.482 | 1.003 |

Age | 64.076 | 60 | -.012 | .010 | 1.509 | .988 |

*** = p < 0.001 ** = p < 0.01 * = p < 0.05 | ||||||

Table 2.

Summary on the added value each variable related with the crime record has on the model. | ||||||

X2 (OMTM) | B | S.D. | Wald | Exp(B) | 95% C.I. | |

Financial Ant. | 11.503** | .702 | .201 | 12.141*** | 2.017 | 1.359 – 2.993 |

Conv. Cases | 1.092 | |||||

Conv. Facts | .379 | |||||

Total All | 3.416 | |||||

*** = p < 0.001 ** = p < 0.01 * = p < 0.05 | ||||||

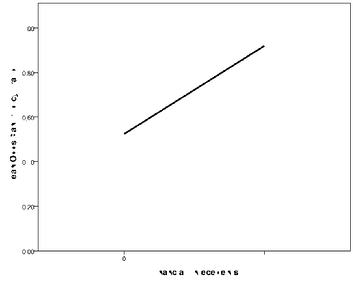

Financial Antecedents have an added value on the model in predicting bankruptcy fraud. The other variables have no added value and do not need further investigation. Exp(B) = 2.017 p<0.0005 meaning that when there are financial antecedents present the odds multiply with 2.017 (Figure 1).

Figure 1.

Relationship between the mean odds of bankruptcy fraud and financial antecedents.

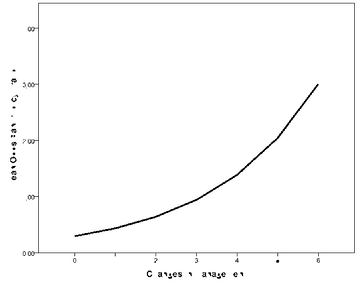

The second hypothesis that can be tested with this group of datasets is the correlation between the number of changes in management and bankruptcy fraud. The ‘Chi square test’ and ‘simple logistic regression’ results can be seen in Table 1. With X2 (6, N = 1474) = 39.595 p<0.0005 there is a highly significant result. The logistic regression consequently gives Exp(B) = 1.473 p<0.0005. A significant result meaning that each change in management increases the odds of fraud with a factor of 1.473. This effect is graphed in Figure 2.

Figure 2.

Relationship between the mean odds of bankruptcy fraud and changes in management the six months prior to bankruptcy fraud.

The last hypothesis that is tested with this dataset is if offenders guilty of bankruptcy fraud are older than non-offenders. There is no significant result between ‘age’ and the probability of bankruptcy fraud ( X2 (60, N = 1474) = 64.076 p>0.05 ).

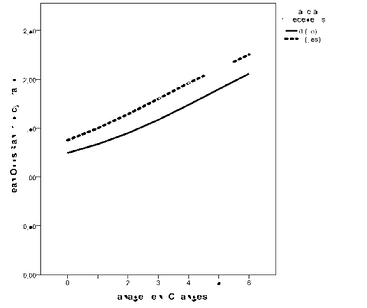

Besides the data that is needed to test the hypotheses there are also other statistical analysis that can be done. First of all it is interesting to examine the two variables that have proven to be significant and see if they can be combined to produce a better model. Just like before we start with the variable that has the strongest effect (Financial Antecedent) and check whether the less strong one (Management Changes) has an added value on the model. The results are shown in Table 3.

Table 3. Summary on the added value each variable has on the model. | ||||||

X2 (OMTM) | B | S.D. | Wald | Exp(B) | 95% C.I. | |

Financial Ant. | 8.977** | .200 | .089 | 6.581 | 1.669 | 1.128 – 2.468 |

Man. Changes | 23.600*** | .077 | .208 | 23.117 | 1.448 | 1.245 – 1.684 |

*** = p < 0.001 ** = p < 0.01 * = p < 0.05 | ||||||

The variable ‘Management Changes’ has a significant added effect on the reduced model. This means that both variables together are a stronger predictor of bankruptcy fraud than either one is on its own. The amount of cases that is correctly predicted by the model does not improve by much though (Table 4.). The results are graphed together in Figure 3. A small piece of the dotted line is missing. This is because there are no companies with five changes in management and a ‘yes’ on ‘financial antecedents’.

Table 4. Percentage of cases predicted correct | |

Percentage Correct | |

Step 0 | 75.4% |

Financial Ant. | 75.4% |

Man. Changes | 75.8% |

Figure 3.

Relationship between the mean odds of bankruptcy fraud, changes in management the six months prior to the bankruptcy and financial antecedents.

Although the second group of data cannot be used to test hypotheses it is interesting to see what results it gives. It is analyzed in the same way as the previous group of datasets. A ‘Chi Square test’ is performed after which all variables are used one by one in a ‘simple logistic regression’ to scan for direction and strength of the effect. The results are shown in Table 5. The variables ‘HKS’ and ‘BPS’ are highly significant.

Table 5. Summary of the effect of independent variables on suspected bankruptcy fraud. | ||||||

X2 | Df | B | S.D. | Wald | Exp(B) | |

H.K.S. | 23.955*** | 1 | 1.470 | .307 | 22.895*** | 4.351 |

B.P.S. | 64.322*** | 1 | 3.146 | .470 | 44.736*** | 23.250 |

M.O.T. | .085 | 1 | .119 | .409 | .048 | 1.126 |

*** = p < 0.001 ** = p < 0.01 * = p < 0.05

To see if these two significant variables have a stronger effect when they are used together multiple logistic regression is used. The results are in Table 6.

Table 6. | ||||||

X2 (OMTM) | B | S.D. | Wald | Exp(B) | 95% C.I. | |

B.P.S. | 71.451*** | 2.993 | .480 | 38.850 | 19.940 | 7.781 - 51.101 |

H.K.S | 11.133** | 1.197 | .364 | 10.798 | 3.309 | 1.621 - 6.756 |

*** = p < 0.001 ** = p < 0.01 * = p < 0.05 | ||||||

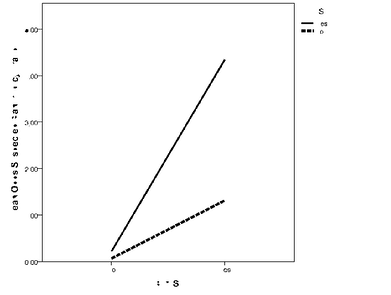

Both variables have an added effect on the probability of suspected bankruptcy fraud. The results are plotted in Figure 4.

Figure 4.

The relationship between the mean odds of suspected bankruptcy fraud and registration in the B.P.S. and H.K.S.

Table 7. Percentage predicted correctly | |

Percentage Correct | |

Step 0 | 51.0% |

B.P.S. | 77.3% |

H.K.S. | 77.3% |

Both variables contribute to a better model. This is shown in the percentage of cases that is predicted correctly by the model (Table 7).

Finally the third group of datasets is examined for results on the variables traffic accidents and ‘driving and drinking’. Because the dependent variable is still categorical we use a Chi Square test and a simple logistic regression test. The results are shown in Table 8.

Table 8.

Summary on the effects of independent variables on bankruptcy fraud. | ||||||

X2 | df | B | S.D. | Wald | Exp(B) | |

Traffic Violations | 17.234 | 13 | .002 | .049 | 0.001 | 1.002 |

Traffic Violat. Cat. | 0.515 | 1 | -.171 | .238 | .515 | .843 |

Drink. and Dr. Off. | 10.996 | 5 | .190 | .175 | 1.185 | 1.209 |

Drink. and Dr. Cat. | 1.454 | 1 | .384 | .320 | 1.443 | 1.468 |

*** = p < 0.001 ** = p < 0.01 * = p < 0.05 | ||||||

There are no significant results on any variables in the last dataset.

Discussion

Bankruptcy fraud is a crime that is difficult to prevent. With the current detection and prosecution rate of 2.5% criminals have little concerns that they will ever get caught. The higher this percentage is raised, the less attractive the crime becomes. It will always be a utopia to detect and prosecute every single case of bankruptcy fraud but by raising the detection rate a step is made to diminish the damage done through this kind of fraud. This study has attempted to help with that goal.

The hypothesis that owners or managers with previous financial antecedents are more likely to commit bankruptcy fraud is confirmed. People that have committed crimes before seem to be more likely to commit them again. It indicates that committing fraud is not something that everyone would do under certain circumstances. People who have committed a financial offence before are more likely to do it again. This points in the direction of a distinct personality which differentiates them from non-offenders. The difference is significant but not very large.

When companies start heading towards bankruptcy there often is a change in management. This can have multiple reasons. An owner who has lost hope of saving the business may sell it to a malefic person. Or a straw men can be installed as owner. This way the original owner tries to get out of his liability. The hypothesis that the amount of changes in the management or ownership the six months before bankruptcy correlate with bankruptcy fraud is indeed true. There is a significant effect but again this effect is not too big.

The two hypotheses can be connected. Most entrepreneurs are honest hardworking men who were not able to turn their luck around and keep their business running. In most cases there is no deliberate intention to commit any kind of fraud. Often another person is needed to do this. It is therefore not surprising that a higher number of changes in management in the six months prior to bankruptcy is an indicator of bankruptcy fraud. The people who come into the business often have had experience with financial antecedents and are not afraid to get in the process of getting financial problems (through the bankruptcy) again. So when someone takes over a company with the intention of deliberately letting it go bankrupt it is likely that it is not the first or last time this person does it. This group is the one that we are most interested in.

Even though these two hypotheses have been confirmed by the data, it only yields a small effect. When the full model is compared to the reduced model there is only a small improvement from 75.4% to 75.8% in correctly predicted cases (Table 4). While this improvement is significant, its effect is small and a consideration should be made whether the extra costs and effort that go into implementing such a model are worthwhile. There are however some unexpected results that are not predicted by the literature.

In the second dataset group suspected bankruptcy is analyzed versus three internal systems. Two of these systems proved to have a significant effect. In contrast to the number of changes in management and the financial antecedents this difference is much larger in comparison to the reduced model. The reduced model only predicts 51% correctly. The full model predicts 77.3% off all cases correctly (Table 7). Like the correlations in the main dataset, this effect is also significant but the influence these variables have on the model is much greater. A side note is in order here though, the dependent variable in this set is not ‘bankruptcy fraud’ but ‘suspected bankruptcy fraud’. Any conclusions that are drawn from these results will have to be done with the notion in mind that there is no certainty that these companies actually did commit fraud. Follow up research should examine how high the correlation between ‘suspected bankrupt fraud’ and ‘actual bankruptcy fraud’ is. If this correlation is sufficiently high than registration in the B.P.S. en H.K.S. are excellent indicators and can truly make a difference in detecting and tackling the problem and raising the detection and prosecution rate.

The hypothesis that offenders score lower on self control than non-offenders was measured implicitly through the number of ‘driving and drinking’ convictions a person had. No significant result was found.

Hypothesis two predicted that bankruptcy fraud offenders would score lower on conscientiousness than those who do not commit fraud. This was measured indirectly by using traffic violations as an indicator for conscientiousness but the results did not support the hypothesis.

The prediction that bankruptcy fraud offenders are older than non-offenders was not proven.

Unfortunately it was not possible to formulate hypotheses about the two types of bankruptcy offenders (the ‘high level’ and ‘low level’ offender). The datasets made no distinction in the kind of bankruptcy fraud, nor was any extra information given about this.

Future Research and Limitations

The single biggest obstacle in the literature study was that most of the research considers white collar criminals as a homogenous population with similar characteristics (Collins & Schmidt, 1993. Blickle et al. 2006. Walters & Geyer, 2004 ) . This practice may well be a misconception. As indicated earlier, white collar crime is an umbrella term. It encompasses several different crimes. In the beginning of this paper we mentioned six categories of white collar crime as defined by Coleman (2002). Each of these categories can have a different kind of offender. For example, the average person who commits employee theft most likely has a different profile than a person who commits a computer crime. Someone who takes or gives bribes or has a conflict of interest can again be different. By neglecting the fact that there are several different kind of white collar criminals out there, researchers risk getting flawed results when they treat all of them as a single group. Because of this tendency to treat all white collar criminals the same it was hard to identify personality determinants that are typical for a bankruptcy fraud offender. Particularly troubling was making a distinction between bankruptcy fraudsters who had no deliberate plan to commit fraud and bankruptcy fraudsters who bought or started a company with the deliberate purpose of letting it go bankrupt. Future research should be thoughtful of these differences and not generalize all offenders in the same class.

There is some researches which focuses on the personality determinants of economic offenders (Alalehto, 2003). This kind of research gives us a glimpse on the personality of white collar criminals. Besides the above mentioned warning that white collar criminals should not be seen as one group but as several different groups there is another problem. While examining the difference between populations of offenders and non-offenders is very interesting, it often does not have a direct practical use. Unfortunately fraudsters do not fill out personality questionnaires for us in advance to use when we please. This makes it difficult to put research findings on the subject to practical use. It is not impossible however. In testing the first hypothesis we just tried to measure conscientiousness by examining the amount of speeding tickets. This is a very crude and unreliable way to measure a personality determinant but it gives an idea on the manner in which results can be applied. Currently some very recent research has come out on narcissism in CEO’s (Rijsenbilt, A., 2011). Rijsenbilt first identifies the influence narcissism can have on fraud sensitivity and then describes how it is possible to ‘measure’ a CEO’s narcissism on the basis of company year reports. In doing so it becomes possible to indicate which companies are at risk for fraud by looking at observable and public data.

Ideally something similar becomes possible for bankruptcy fraud too. By knowing in what way bankruptcy fraud offenders differ from their non fraudulent colleagues we can search for systematic anomalies in company data or personal bio data (of the managers/owner) that are an indication for these differences. When observable features are identified Elliot’s (2010) criticism that use of the ‘Big Five’ model is too theoretical and too difficult to measure to be used in practice can be overcome by using implicit measures of personality characteristics.

A challenge for the future is to find observable differences between the ‘higher level’ fraudster and the ‘lower level’ ones. The ‘higher level’ fraudsters are considered the biggest problem. Further research should be done to find out what typical characteristics this type of criminal has and how these differ from ‘lower level’ offenders and non-offenders and how this can be detected by using directly observable data. An interesting personality trait to consider is machiavellianism. This trait is not one of the ‘Big Five’ but rather comes from a concept called the ‘Dark Triad’ (Paulhus, D. L., & Williams, K. M., 2002). Machiavellianism has been associated with fraud (Dion, 2010) and future research might be aimed at exploring the correlation it has with bankruptcy fraud and especially if it correlates more with its ‘higher level’ form.

On a final note regarding limitations, when trying to generalize the results of this study, one should be careful in doing so. Data was collected regionally. Therefore, although there is no reason to suspect so, results in other parts of the Netherlands or in other parts of the world may differ. Generalizing these findings should only be done after careful consideration of all relevant factors and even then still with caution.

Conclusions

Unfortunately no significant results turned up regarding personality traits or bio data.

A significant effect did present itself between the amount of changes in management and financial antecedents with respect to bankruptcy fraud. However, this effect does not increase the detection rate by much. When contemplating whether or not the findings of this model should be implemented in practice a consideration should be made whether the costs are worth the benefits. The analysis of the internal registration systems ‘HKS’ and ‘BPS’ on the other hand give effects that are a lot stronger. Keeping in mind that the dependant variable here is ‘suspected bankruptcy fraud’ further research should be done to determine the correlation with ‘actual bankruptcy fraud’ but this effect is so strong that it should not be overlooked and may well prove to be influential in the fight against bankruptcy fraud.

References

Alalehto, T. (2003). Economic crime: Does personality matter? International Journal of

Offender Therapy and Comparative Criminology , 47, 335–355.

Almagor, M., Tellegen, A., &Waller, N. G. (1995). The big seven model: Across-cultural

replication and further exploration of the basic dimensions of natural language trait

descriptors. Journal of Personality and Social Psychology, 69, 300-307.

Arthur, W., & Graziano, W.G. (1996) The five-factor model, conscientiousness, and driving

accident involvement. Journal of Personality, 64, 593–618.

Benson, M.L., & Simpson, S.S. (2009). White-Collar Crime: An opportunity perspective. New

York: Routledge.

Blickle, G., Schlegel, A., Fassbender, P., & Klein, U. (2006). Some personality correlates

of business white-collar crime. Applied Psychology: An International Review, 55, 220–233.

Coleman, J.W. (2002). The criminal elite: Understanding white-collar crime (5th ed.).

New York: Worth Publishers.

Collins, J.M., & Schmidt, F.L. (1993). Personality, integrity, and white-collar crime:

A construct validity study. Personnel Psychology, 46, 295–311.

Edelhertz, H. (1970). The nature, impact and prosecution of white collar crime, U.S.

Department of Justice.

Elliot, R.T. (2010). Examining the relationship between personality characteristics and

unethical behaviors resulting in economic crime. Ethical Human Psychology and Psychiatry,

12, 269.

Friedman, M., & Rosenman, R.H. (1994). Type A behavior and your heart . New York: Knopf.

Keane, C., Maxim, P.S., & Teevan, J.J. (1993). Drinking and driving, self-control, and gender:

Testing the general theory of crime. Journal of Research in Crime and Delinquency, 30, 30-

46.

Knegt, R., Beukelman, A.M., Popma, J.R., van Willigenburg, P., & Zaal I., (2005). Fraude en

misbruik bij faillissement: Een onderzoek naar hun aard en omvang en de mogelijkheden

van bestrijding. Amsterdam: Hugo Sinzheimer Instituut.

Kolz, A. (1999). Personality predictors of retail employee theft and counterproductive

behavior. Journal of Professional Services Marketing, 19, 107–114.

Ones, D.S., & Viswesvaran, C. (2001). Integrity tests and other criterion-focused occupational

personality scales used in personnel selection. International Journalof Selection and

Assessment, 9, 31–39.

Paulhus, D.L., & Williams, K.M. (2002). The dark triad of personality: Narcissism,

machiavellianism, and psychopathy. Journal of Research in Personality, 36, 556 –563.

Pogrebin, M., Poole, E., & Regoli, R. (1986) Stealing money: An assessment of bank

embezzlers. Behavioral Sciences and the Law, 4, 481–490.

Ragatz, L., & Fremouw, W. (2010) A critical examination of research on the psychological

profiles of white-collar criminals. Journal of Forensic Psychology Practice, 10, p 373-402

Rijsenbilt, A. (2011). CEO narcissism; measurement and impact. Retrieved June 28, 2011,

from the Erasmus Research Institute of Management – ERIM.

Smith, T.R. (2004). Low self-control, staged opportunity, and subsequent fraudulent

behavior. Criminal Justice and Behavior, 31,542-563

Skaar, N.R., & Williams, J.E. (2005) Gender differences in predicting unsafe driving behaviors

in young adults. Cedar Falls, Iowa, USA. University of Northern Iowa

Sutherland, E.H. (1940). White-collar criminality. American Sociological Review, 5, 1–12.

Veldkamp, B.P., & de Vries, T. (2008). Identification of bankruptcy fraud in Dutch

organizations. Retrieved may 21, 2011, from University of Twente.

Walters, G.D., & Geyer, M.D. (2004). Criminal thinking and identity in male white collar

offenders. Criminal Justice and Behavior, 31, 263–281.

Zahra, S.A., Rasheed, P.A.A., Shaker, A., & Richard, L. (2007). Understanding the causes and

effects of top management fraud. Organizational Dynamics, 36, 122–139.